Things I Think I Think - Q2 2026

There is a magical time once every 4 years when the world comes together around the beautiful game. Given all of the geopolitical changes that have taken place over the past few years, it’s hard not to smile at the fact that cohost United States will play its first elimination game today, on Canada Day, while Canada will next take to the pitch on the 4th of July.

Let’s go Canada! 🇨🇦

Set against the backdrop of this summer’s competition for global sport supremacy, here are 5 Things I Think I Think - Q2 2026 Edition:

1. Fast and then Slow

The frantic pace of investment that characterized the first quarter of 2026 continued into Q2. Megafunds, in particular, continued to throw around their proverbial weight, with numerous preemptive rounds happening at the start of the quarter (especially at Series A and B). I suspect that when the statistics for Q2 eventually see the light of day, we’ll see that valuations for the top 5% of companies continued to climb sharply through Q1 and into Q2.

But a funny thing happened as May rolled around: the pace of deals started to slow. Gradually, then suddenly.

In particular, the preemption of Series A and B rounds that was prevalent during the first third of the year dropped off rather dramatically towards the end of Q2. I watched a number of VCs that had been aggressively pursuing preemptive deals downshift their activity mid-quarter. Almost in sync, a number of founders I know who were looking down the barrel of preemptive term sheets stepped back from the alter, with plans to revisit in the fall.

It’s not often that you see VCs and founders adjust their activities in parallel. In my inaugural “Things I Think I Think” post back in 2023, one of my observations was about Canadian founders lagging in their acceptance of and adjustment to changes that were happening in the market post-ZIRP. So what happened in Q2 was quite unusual (but something I view as a strong positive). It wasn’t so much a correction in the fundraising market as a mutual, unspoken agreement by both sides to hit the pause button.

Coming into Q2, I had spoken with both VCs and founders who felt that they had no choice but to play the “preemption game”. As alluded to in my Q4 2025 update, investors fearful of missing out on the next OpenAI or Anthropic were driving “…a degree of preemption and FOMO for hypergrowth AI startups that’s on par (if not greater) than what happened during ZIRP.” At the same time, a number of founders I spoke with felt like they had an obligation to entertain preemptive investor interest. Many of them were spending considerable cycles on investor meetings even though they already had plenty of money in the bank.

By the time June came around, the slowdown in activity had expanded well beyond the “cease fire” in preemptive investments. Many VCs I know — from Pre-Seed to Series B — had all but stopped taking new meetings by the start of June. Perhaps it was a similar desire to hit pause and revisit their AI-related investment theses. Perhaps it was simply a weariness after more than a year of frenetic activity. Regardless, this summer is going to be a particularly bad time to fundraise (but a great time to be heads down on your business).

2. The IPOs are Coming! The IPOs are Coming!

Q2 saw the first of three potentially massive tech liquidity events with SpaceX’s record-breaking IPO. But it was the other two IPOs on the horizon — from Anthropic and OpenAI — that had a more immediate impact on the behavior of many VCs.

As I alluded to above, a lot of the high-octane investor behavior over the past year has been driven by VCs desperately trying to replicate investments in Anthropic and OpenAI. Both companies have achieved unprecedented user adoption, revenue growth and — most appreciated by investors — valuation growth (aka markups). And, until recently, both seemed on a path that would quickly translate those paper gains into similarly unprecedented IPOs (DPI!).

But what seemed like surefire wins suddenly became not-so-certain. Anthropic’s smooth sailing hit bumpy seas as it repeatedly found itself in conflict with the U.S. government, while ongoing questions about OpenAI’s business fundamentals has led to speculation that it may delay its IPO until 2027.

Pete the Cat, early-stage VC

As the shine began to come off these two industry darlings, VCs slowly started to remove their rose-colored AI glasses. The slowdown in preemptive activity I described above was very much triggered by the recognition that, despite their unprecedented growth trajectories, the path from inception to IPO for AI-based companies is still a bumpy one.

To be clear, investors are by no means giving up on AI (many are still wearing very thick rose-colored AI glasses, albeit with a slightly lighter tint). The fact that Anthropic and Open AI have hit bumps in the road won’t damper VC enthusiasm for AI’s industry-disrupting potential. Rather, investors are adjusting their expectations when it comes to the trajectories of these companies, particularly as it relates to time-to-liquidity. Ultimately, that will affect the rate at which preemptive rounds occur and the valuations at which those rounds happen.

But make no mistake, once fall comes around, VCs will once again be champing at the bit to invest in the latest-and-greatest AI startups.

3. Agents Cross the Chasm

When I wrote my end-of-year update six months ago, nobody had heard of moltbot clawdbot OpenClaw. By Q1, prominent VCs were showing up on podcasts wearing lobster costumes. But the technology was still barely usable. We were still very much at the Homebrew Computer Club phase of the technology adoption lifecycle.

But like many things related to AI, the rate of progression from barely usable open source “projects” to relatively-stable early “products” has been unprecedented. This past quarter, a number of companies came to market with purpose-built agent products, ranging from more mature open source projects, like Hermes, to agents for managing family calendars. Howie, an email scheduling assistant that I previously wrote about, recently released “Howie Blue”, a full-blown personal agent that integrates with both email and iMessage (hence the name).

My friend Hiten did a great job of describing the value that many early adopters got from working with nascent agent platforms, though I’m not sure that the general populace had nearly as much ROI to gain from adopting the technology so early. But with so many agent-based products now coming to market, the bar has never been lower to start using AI agents.

I expect that adoption rates of agent-based products will skyrocket as we head into the back half of the year, especially in Startupland™. For founders and investors alike, the takeaway should be this: if you aren’t already using agents in some form or another (not just within your company, but you personally) take some time this summer to get started. It doesn’t matter if you’re rolling your own open source agent or signing up for one of the many turnkey solutions hitting the market. Do something.

Continuing to sit on the sidelines won’t land you in a “permanent underclass” (despite what many in Silicon Valley continue to believe), but it will absolutely leave you at an increasing competitive disadvantage.

(If you’re not sure where to start, I recently wrote about how I’ve used agents to prioritize the important-but-not-urgent. If you need even more of a nudge, use this link to get $20 off any Howie.ai plan — I’m not an investor in Howie, just a really big fan.)

4. Canadian VC on the Brink

For the past few quarters, the ongoing bifurcation of venture capital has led to a relatively small number of big VC firms capturing an increasing percentage of LP dollars. This shift is happening all over the world, but the particular manner in which it has manifested in Canada has the potential to completely devastate the country’s tech sector.

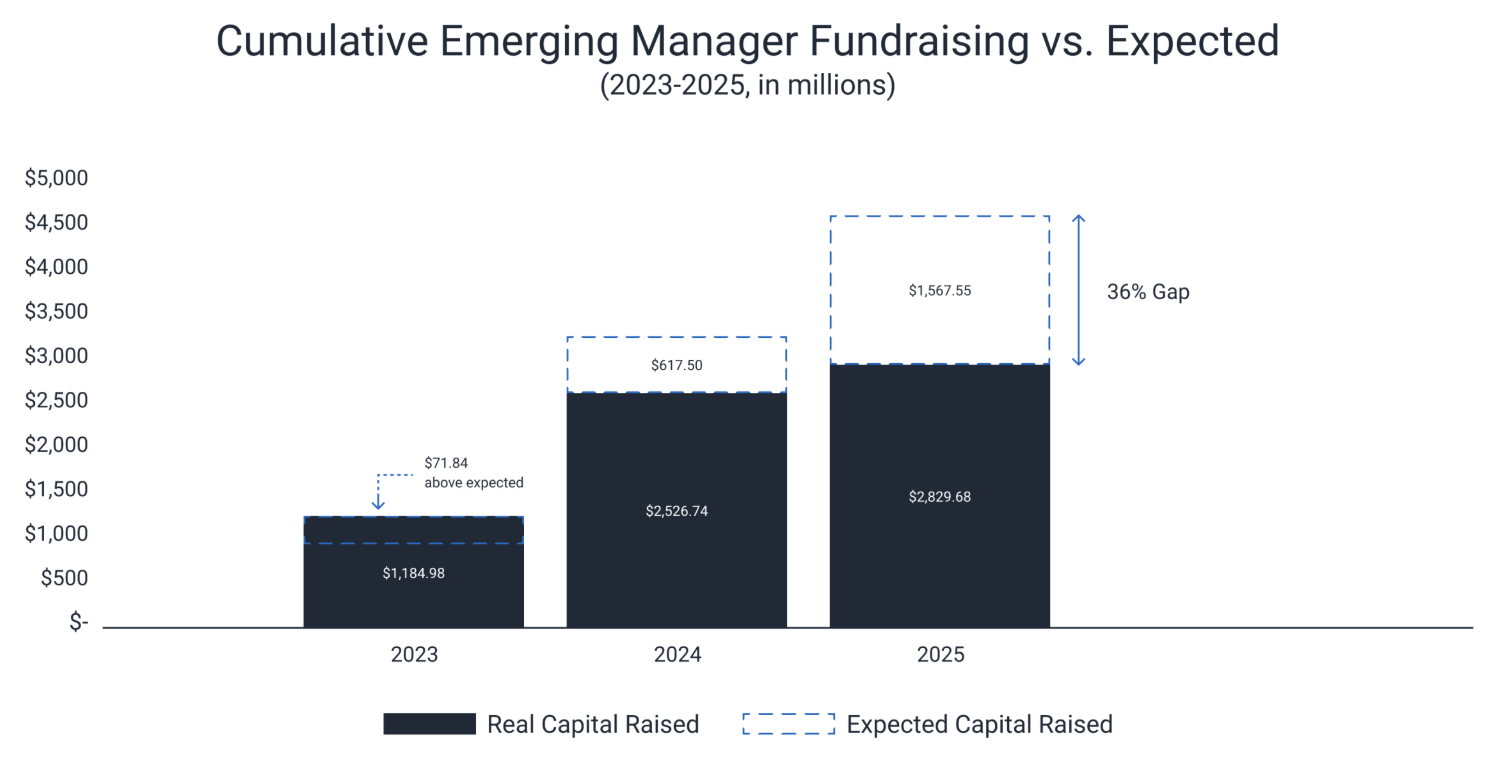

RBCx recently published its mid-year report on Canada’s VC market, which included a staggering claim: as of the end of 2025, the country’s emerging managers (new VCs who are on their first, second or third fund) have raised 36% less capital than projected. For a country that already has too few early-stage VCs, a lack of fundraising by emerging managers is nothing less than an existential threat to its entire tech sector.

A lack of support for emerging managers isn’t a new phenomenon in Canada. In fact, I wrote about it 3 years ago. But the implications of the current prolonged drought has the country on the precipice of disaster — whether or not its leaders realize it.

Why? Emerging managers overwhelmingly invest at the earliest stages. They also tend to bring new ideas and new perspectives to startup ecosystems. That frequently leads them to be the first check into companies with very different profiles to what “old guard” VCs back, which is key to an ecosystem’s ability to innovate and drive long-term growth. Lisa Cawley, Managing Director of Screendoor, a leading fund-of-funds that invests exclusively in U.S.-based emerging managers, described the critical role of new VCs to the Wall Street Journal last year,

“New VC firms matter; they have an opportunity to drive competition and disrupt incumbent complacency. The question shouldn’t be ‘How many VCs,’ but why are there so many mediocre ones?”

That said, a dip in the number of early-stage VCs in an ecosystem typically doesn’t threaten its long-term survival. But time is not on Canada’s side. Its unique existential threat comes from the fact that its neighbor to the south is home to the tech world’s largest, fastest-moving and most risk-taking capital market. At a time when fewer Canadian VCs are willing (or able) to write the first check into first-time founders, a growing number of local founders have simply stopped looking for capital at home. Instead, they’re going straight to Silicon Valley.

And in many cases, those first-time Canadian founders are choosing to move to the U.S. as part of the process.

A handful of efforts have recently emerged trying to address the lack of capital flowing to emerging managers in Canada — notably the launch of the Canadian Startup Capital Association (CSCA) in April — but the country needs to make some bold, systemic moves fast. The last time Canada experienced a dip in the number of active VC firms, most Silicon Valley VCs were unwilling to invest in Canadian startups. That’s no longer the case.

If 2026 ends with a similar lack of fundraising success for Canada’s emerging managers, by this time next year there may not be much of a startup pipeline for the rest of the ecosystem to support.

5. We Lost a Giant

Last week, Om Malik passed away after a prolonged health battle. Countless posts and articles have been written about him in the days since. This observation from John Gruber does a good job of capturing how many of us in the tech industry currently feel,

“it is a profound irony that a man with such a big and beautiful figurative heart could have such a lousy literal one.”

I only met Om a handful of times over the years, so I can’t say that I knew him well, but his work and legacy had a profound impact on my journey.

His namesake publication, Gigaom, was unlike any other tech publication at the time (or since). It seamlessly blended the “breaking news”-style coverage of Silicon Valley that was on the rise with a deeper level of analysis — about both technology and business — that simply didn’t exist anywhere else. The approach stemmed from Om’s personal style of journalism, which Stacey Higginbotham described thusly,

“He was the smartest guy writing about really geeky tech and putting it into context. He was able to discuss the nuts and bolts of technology and then extrapolate what new advances would mean and how people would react.”

Gigaom focused primarily on infrastructure and enterprise software, which put both Aster Data and DataHero squarely in its coverage box. In 2009, the publication brought on a dedicated infrastructure/data writer named Derrick Harris, who I quickly got to know and soon became friends with. He shared his own thoughts on Om’s passing here.

For more than 5 years, my professional world existed very much within the orbit of Gigaom. I got to know many of the exceptional writers that passed through its doors and had the privilege of speaking at several of the company’s influential conferences. To this day, the way in which I view tech journalism and its potential for positively influencing the world while holding people in power accountable is overwhelmingly influenced by my years interacting with the team at Gigaom.

In a world where tech media is increasingly driven by algorithms and agendas, the type of deep, thoughtful writing that Om championed is frustratingly hard to come by. If you haven’t already checked out Crazy Stupid Tech, the blog Om launched last year with Fred Vogelstein, I strongly encourage you to do so.