Things I Think I Think - Q1 2026

Three months ago, nobody had heard of moltbot clawdbot OpenClaw, OpenAI was valued at a mere $500B, and Anthropic was signing multi-year partnerships with the U.S. Government.

Here’s where we stand ninety days into 2026 in my latest homage to legendary sports columnist Peter King.

Try explaining this one to 2025 Garry

Here are 5 Things I Think I Think - Q1 2026 Edition:

1. The Bifurcation of VC Continues (Continued…)

In my Q4 2025 post, I shared some observations about the ongoing bifurcation of VC. In particular, I discussed some of the changes that were starting to emerge at the Seed round. Over the past three months, those shifts have gone into overdrive.

It’s now very clear that for a certain category of companies (namely, AI-native companies whose revenue tracks usage), the growth trajectory is very different from what has historically been the case in the software world. The extreme compression of time has led to a dramatic acceleration of funding for those companies and a dramatic upswing in round sizes and valuations. And while usage-based revenue won’t last forever, the companies capitalizing on it are running away from the proverbial pack.

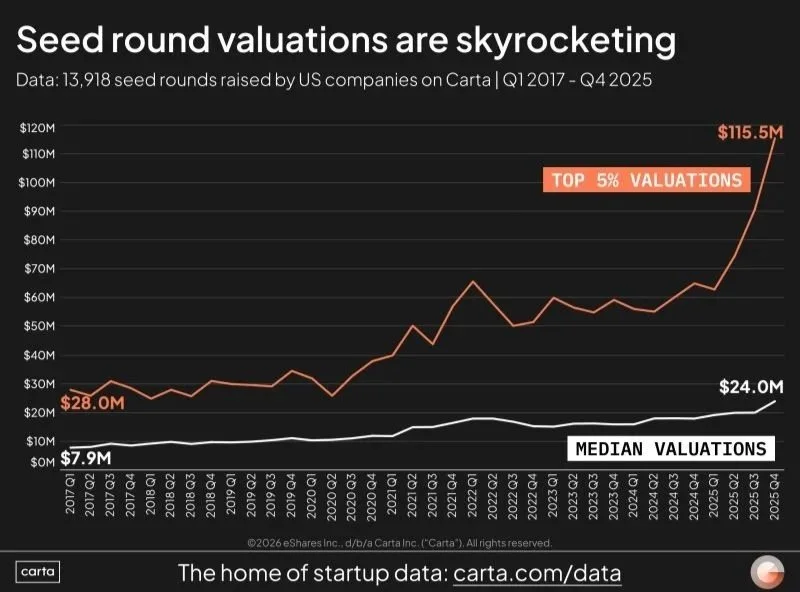

Carta recently noted that the top 5% of U.S. Seed rounds in Q4 2025 had an average valuation of $115.5M (compared to a median valuation of $24M). That looks a lot more like a traditional Series A valuation. And if this year’s on-the-ground activity is any indication, I expect the Q1 numbers to absolutely crush that.

So, if it’s the case that the top segment of Seed companies are splitting off from the rest, are we still talking about a “bifurcation” of VC?

Yes.

Because it’s the megafunds that are swooping in to fund the perceived top Seed companies.

The vast majority of traditional Seed funds (even large ones) can’t afford to invest in these mega rounds. At least…not with traditional fund models. Which is why we’re seeing a ton of adjustment happening amongst Seed VCs. I shared some thoughts on this shift in last week’s post, but it’s worth pointing out that we’re only just starting to see the resulting dominos fall.

I expect that we’ll see a lot of changes when it comes to fund strategies at the Seed by this time next year. In particular, I expect that we’ll see a number of Seed funds adjust their models to look more like Pre-Seed microfunds, with 3 - 5% ownership targets at much higher valuations.

In the meantime, I offer a warning for founders preparing to fundraise: expect to see a Seed crunch for at least the rest of this year.

Much like the Series A crunch we saw last year, this one won’t be due to a lack of capital. It will be because the majority of Seed funds are completely rethinking their investment criteria.

Warning: goal posts moving

In the past few weeks alone, I’ve seen multiple companies that would have easily raised a Seed round a year ago struggle to get first meetings with VCs. Companies with real revenue and prominent logos aren’t even getting a 20-minute intro call.

Plan accordingly.

2. The SF Maker Phase is On Off On

A little over a year ago, I noted that the “maker faire” phase of San Francisco’s AI cycle was over,

“…we’ve moved from the “innovators” phase of this edition of the San Francisco technology lifecycle to the “early adopters” phase. And that’s a good thing.

This isn’t to say that you shouldn’t go to San Francisco in 2025 if you’re a builder — you absolutely should — just don’t expect it to have the same level of serendipity as last year. On the other hand, if you’re a founder a bit further along on your journey who’s looking to meet other high-quality founders focused on building their companies, there’s no better time to come. Just know that you need to be more intentional about your visit and manufacture the outcomes you want.”

I also argued that, “if history’s any indication, it will be another 20 years before it’s back.”

It turns out that history wasn’t helpful in this one. In January, moltbot clawdbot OpenClaw took the tech world by storm. Add to that the latest advancements in Claude Code and it seems like everyone is back to tinkering again.

In reality, I don’t believe that we’re heading back to another full-blown “maker faire” phase of SF’s tech cycle, but there is definitely is mini boom that’s happening right now around agents. Lots of meetups. Lots of activity. Lots of enthusiasm.

I suspect that this maker revival period will be relatively short-lived, particularly as more (and differently-targeted) agent offerings come to market. But it’s definitely going to be an eventful spring in Silicon Valley.

3. Do You Even Moat, Bro?

Another ongoing debate in the tech world surrounds the evolution of moats.

Historically, technical moats were a big deal for a lot of VCs. But with AI compressing time-to-market, a variety of new ideas have emerged. Some pundits have argued that deep knowledge of a particular industry or specialization will be a moat. Others suggest that trust and brand loyalty will win the day. There’s also the element of “taste”…

Jordi Visser recently wrote an article titled, The Repricing of Time: Equity in the Age of Agents, in which he discussed the impact of AI on equity markets (I highly recommend that you read it). Jordi posits the following:

“For more than a decade, equity markets were built around a simple premise: durable franchises deserved durable multiples. Investors weren’t just buying earnings. They were buying time. Time to compound. Time before meaningful competition arrived…Time was the moat.

…

But something subtle has changed.

AI does not simply disrupt business models.

It compresses time.”

Jordi goes on to propose that as AI continues to improve, the biggest moat will no longer relate to what you are building. It will be dictated by your ability to adapt. In other words, more than ever before, velocity will be the one metric that matters most.

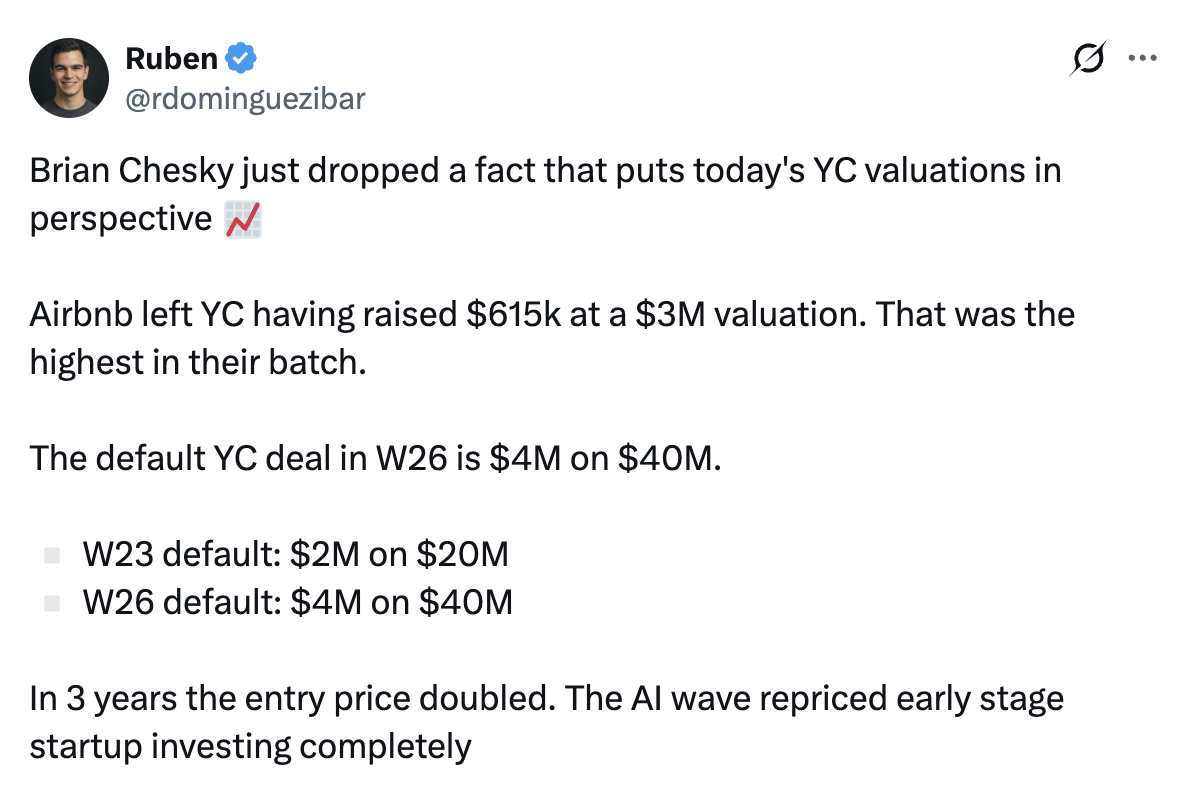

4. YC is Pricing the Market

A year and a half ago, I noted that YC was boxing out. Earlier that year, Techstars had effectively failed. With 500 Startups’ having imploded a few years prior, that left an unprecedented opening for YC to dictate the proverbial terms across the entire accelerator landscape. It started with a move to 4 batches per year and has followed with the firm driving higher and higher average valuations each batch.

To be clear, the “default” YC deal isn’t actually what all of the companies graduating from the program get. (Moreover, as an index YC batches represent a very particular segment of the early-stage market — one typically characterized by high-pedigree founding teams supplemented by certain early traction signals). But the fact remains that these companies consistently price at the high end of the market across multiple dimensions.

a16z is targeting the same founder demographic with their Speedrun platform. The firm spent Q1 aggressively ramping up their team (I did more than a few reference calls over the past few months). It will be interesting to see where their batch valuations land as that platform settles into its groove and whether or not the well-funded competition puts a dent in YC’s ability to dictate prices.

5. The Delta Between SF / Silicon Valley and the Rest of the World is Exploding

I constantly travel between San Francisco / Silicon Valley and other startup ecosystems around the world (particularly those in Canada and the UK). Over the past year, the rate of change in the Bay Area has accelerated dramatically. Over the past 3 months, it’s gone stratospheric.

And founders / investors / ecosystem builders in the rest of the world — including in most of the US — genuinely have no clue.

I find myself increasingly disoriented as I bounce between ecosystems. I regularly meet founders outside of Northern California who are excited about the projects and products they’re working on, completely oblivious to the fact that companies in Silicon Valley have long-since abandoned those approaches, technologies or markets. At the same time, technologies that have permeated the day-to-day lives of Bay Area residents are still foreign in most of the world.

That’s certainly not to suggest that founders / startups / investors in the Bay Area are the preeminent experts on everything to do with technology (Silicon Valley remains a very thick bubble in both positive and negative ways). But it feels to me as though the rate of change occurring as a result of AI is actually decreasing the flow of information from Silicon Valley to the rest of the world.

Things are advancing so quickly that people in the Bay Area are finding less time to share what they’re working on with the world outside.

More than ever, I think it’s essential that founders, investors and ecosystem supporters around the world make a point of traveling early and often to Silicon Valley. To understand what’s going on, to benchmark the velocity at which it’s happening, and to understand what the competitive landscape really looks like.

Things are only going to get faster.