What’s Going on with Seed Rounds?

As we near the end of the first quarter of 2026, yet another major shift is underway in the funding / fundraising landscape. And this time, it’s throwing off founders, angel investors, and Pre-Seed VCs alike:

Seed VCs are increasingly not acting like Seed VCs.

“Let’s see who this “early-stage VC” really is!”

Rather than dive into a full history of early-stage investing, I’ll anchor this post with the following loose — but by no means dogmatic — definitions of early-stage VCs (at least, as we’ve come to define them over the past decade or so):

Pre-Seed: The first institutional round of capital. Often comes before any revenue or pilots. The investment decision is primarily based on an evaluation of the team, their initial idea, and its market potential.

Seed: The first round of capital where traction plays a factor in the investment decision. Initial traction (revenue, pilots, etc.) provides early evidence that the product solves a real problem in the market and that customers are willing to pay to solve that problem.

Series A: The first round of capital where traction is at the forefront of the investment decision. At this point, there is enough traction to demonstrate that there is a real market for the product and that initial traction wasn’t a “fluke”. The investment decision focuses on how large and how fast the company can scale its early wins.

To frame it another way, the key variable around which the investment thesis is built for each of these stages is:

Pre-Seed: Team

Seed: Market Hypothesis

Series A: Traction

The Market Hypothesis

If you are unfamiliar with the term “market hypothesis”, it’s the statement that underpins a startup’s primary focus and typically takes the following form:

“There is a market X in which problem Y exists and customers are willing to pay for solution Z.”

If this concept seems vaguely familiar, it’s because of its close relationship to product-market fit (PMF). One definition for product-market fit is the point at which a market hypothesis is proven to be true (through the creation of a product/solution that slots into the hypothesis statement):

“There is a market X in which problem Y exists and customers are willing to pay for our solution Z.”

At the Pre-Seed stage, a market hypothesis may or may not be fully formed. Even if it is, investors typically incorporate into their investment decision an expectation that one or more aspects of it may turn out to be incorrect (and, thus, focus primarily on the team and their ability to iterate in search of product-market fit).

At the Seed stage, the market hypothesis is (historically) at the center of the investment decision. While it may not be in its final form, VCs evaluate potential investments through the lens of the market hypothesis that founders provide. Do they believe that the market is big enough? Do they believe that the startup has the right team to go after that market? To what degree does the early traction support the notion that their solution (a) solves the problem the founders are describing, and (b) demonstrates that customers are willing to pay for that particular solution?

(This is why it’s so important that founders spend time refining their positioning and market hypothesis before fundraising!).

What Has Changed?

While Seed-stage investments have been anchored around the market hypothesis for more than a decade, in the past few months things have shifted considerably. And the reason starts and ends with “AI”.

AI is changing so many things at such a high velocity that many Seed VCs are struggling with how to evaluate startups when they no longer have conviction that the market hypothesis will hold over their 7-10 year investment horizon. Consider the following:

“There is a market X…” — will that market still exist in 10 years?

“…in which problem Y exists…” — will this still be a problem in 10 years?

“…and customers are willing to pay for our solution Z” — will they still be willing to pay for this in 10 years?

Live footage of a Seed VC

While the above comments might seem facetious, it’s important to understand that these are real questions within the context of the role that Seed VCs have historically played. For the past 10+ years, Seed VCs have been primarily responsible for funding companies from the point at which they had a clear market hypothesis and early signals supporting that hypothesis through to product-market fit.

What happens when Seed VCs can no longer rely on those market hypotheses being stable?

How Seed VCs are Reacting

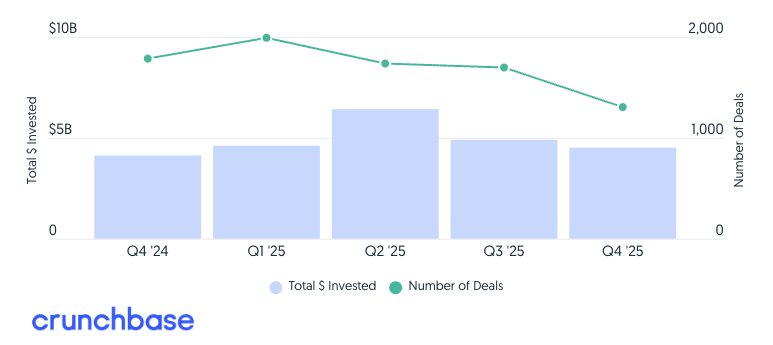

According to Crunchbase, the number of Seed deals in North America has fallen for 3 consecutive quarters — despite the fact that total deal volume by dollars remaining relatively strong. That means capital is concentrating at the Seed stage.

In other words, fewer deals are happening with larger average deal sizes.

North American Seed Investment Through Q4 2025

Beneath the surface, Seed VCs are broadly reacting in one of three ways:

1. Reducing the Number of Deals

Some Seed VCs have reacted by doing fewer deals.

Over the past few months, I’ve spoken with a number of institutional LPs concerned by the fact that some of the funds they’ve invested in aren’t actively deploying capital. One early justification was the need to “slow things down” while they adjusted their investment theses to an increasingly bifurcated VC landscape. But at this point, it appears that some Seed VCs remain inactive / less active because they are simply unsure of what to do.

2. Chasing Repeat / Pedegreed Founders

Many Seed VCs are reacting by investing more in repeat founders and/or founding teams with a strong “pedigree” (graduated from top schools, worked at prominent companies, YC graduates, etc.).

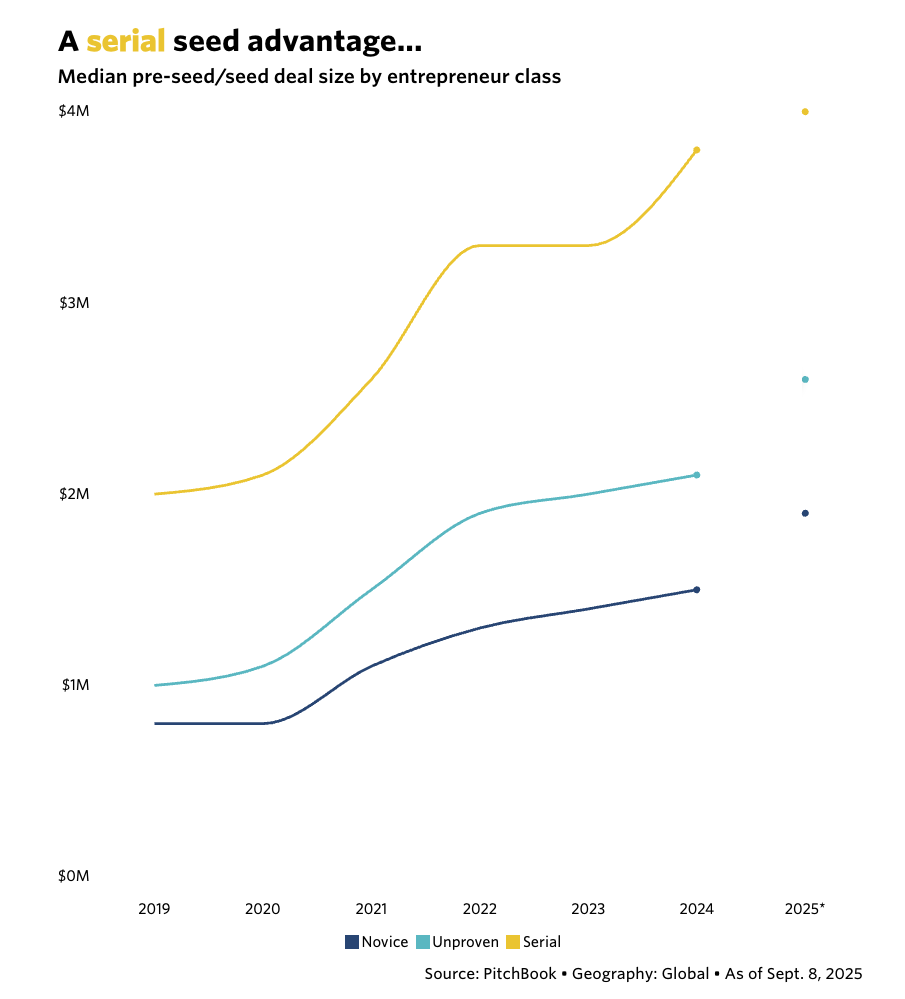

Pitchbook showed a significant increase in the early-stage deal sizes commanded by repeat founders in recent years (in the chart below, “serial” founders are repeat founders who had an exit, while “unproven” founders are repeat founders whose prior companies failed).

In the absence of conviction about the underlying market hypothesis, these investors are betting on the prior experience of the team.

“They figured it out before, so (hopefully) they can figure it out again.”

3. Focusing on Early Traction

The third trend has been to chase signs of early traction.

Early, disproportionate traction has always been something of a cheat code for startups. At the Pre-Seed stage, we often see deals happen quickly when a team comes to the table with unusually strong traction (revenue, users, GitHub stars, etc.), even if they don’t have a fully-formed market hypothesis.

The bet here involves a similar benefit-of-the-doubt as the one given to repeat founders:

“They figured out how to get to X traction, so (hopefully) they can leverage that to build a real product / get to product-market fit.”

Wait a Minute…

Ok, so to summarize what we’re currently seeing in the early-stage fundraising market:

Pre-Seed VCs generally discount the market hypothesis and focus primarily on the team and their ability to iterate in search of product-market fit

Seed VCs are increasingly discounting the market hypothesis and…focusing primarily on the team and their ability to iterate in search of product-market fit???

That’s right. Seed VCs are increasingly acting like Pre-Seed VCs when it comes to their investment decisions.

There’s a lot to unpack when it comes to the potential long-term implications of this shift. It’s especially fascinating within the context of the ongoing bifurcation of VC (and explains why some Seed VCs continue to sit on the sidelines — they simply don’t know how to invest based solely/primarily on the potential of a team). For now founders, angel investors and Pre-Seed VCs need to understand the following about what’s happening at the Seed stage:

Outside of markets that are unlikely to be disrupted by AI, the rubric with which many Seed VCs are evaluating potential investments has changed. Specifically,

The focus on traction has increased — not because it shows more evidence in support of the market hypothesis, but because it shows more evidence in support of the team’s ability to execute.

The focus on a team’s track record has increased.

The impact of whether or not a company is building in a “hot space” has increased.

While Seed VCs are increasingly acting like Pre-Seed VCs, it’s not exactly the same as raising another Pre-Seed round.

For starters, Seed VCs have a lot more data to analyze about your team and your trajectory (especially when it comes to velocity, the one metric that matters most).

It’s also important to understand that Seed VCs have promised their LPs a shorter path to returns than Pre-Seed VCs. In other words, they still need to get an exit in the same amount of time that they did before. This means that you have to be able to demonstrate meaningful progress towards something valuable (it’s not a do-over if you’re still wandering around in the woods in search of PMF).

Finally, this dynamic is most prominent with generalist Seed VCs. Specialized Seed VCs — particularly those in deep tech — are relatively unchanged in their behavior.

If you’re preparing to raise a Seed round, keep the following in mind as you fine-tune your pitch: in addition to analyzing the usual details on problem, solution, traction, etc., many Seed VCs are now asking themselves the following question as part of their investment process:

Can this team win (generate a return) even if one or more of their core assumptions is disrupted by AI? (In other words, can they still win if their market hypothesis gets disrupted?)

Unfortunately, it’s not at all clear yet how Seed VCs are testing for this. As a result, I suspect that we’re going to see a significant “crunch” at the Seed stage in the next few quarters. Startups that historically could raise funding based on a clear market hypothesis and reasonable early traction will struggle, especially if they can’t convince investors that the market hypothesis is viable over a long-term horizon.

Most Seed VCs don’t know what the future is going to look like, so they’re increasingly betting on founders who they believe can figure-it-out.