Hunters vs. Farmers

Over the years, I’ve interacted with hundreds of VCs — first as a founder and, later, as an investor myself. And I’ve heard hundreds of investors pitch their funds. There is a distinct bifurcation in how VCs approach investing and, if you listen carefully to the words they choose to describe themselves with, that approach shows through.

The two approaches are known as “hunting” and “farming”.

I’ve written before about hunting vs. farming within the context of how investors generate returns. In venture capital, “hunting” refers to going out and winning new deals (investing in new companies) while “farming” refers to increasing the likelihood that a company will succeed through post-investment support and services. In theory, investors should do both. In reality, VCs operate across a spectrum, with most firms focusing their efforts on one or the other.

I was recently at an investor conference filled with emerging managers (the VCs behind new, up-and-coming firms). As I listened to pitch-after-pitch from these aspiring VCs, it dawned on me that most founders probably don’t know how to recognize the signs that indicate if an investor is a hunter or a farmer. All VCs seems to use the same “value add” language when talking about why their fund is special, so how can you actually tell?

And why does it matter?

The Difference Between Hunters and Farmers

At a high level, “hunters” are VCs who spend most of their time and effort trying to get into the best deals. For the most part, they focus on companies that are (or will become) “consensus investments” — startups that at subsequent stages will be the hot companies that follow-on investors fight to get into.

Early-stage hunters focus on pedigree and traction as their primary signals. Things like:

Graduating from a top school or program (Stanford, MIT, Waterloo, IIT Bombay, Thiel Fellowship, etc.)

Early employees that left “hot” companies

Repeat founders

Hot sectors

Virality / significant early traction

They’re generally betting on the correlation between pedigree and outcome (or, at least, pedigree and quick markups).

Farmers, on the other hand, tend to cast a wider net. They’re betting on their ability to identify high-potential, non-consensus companies/founders and help them outperform. It’s not that farmers won’t invest in “hot” companies or founders with pedigree. It’s that they believe their edge comes from looking beyond those traditional signals.

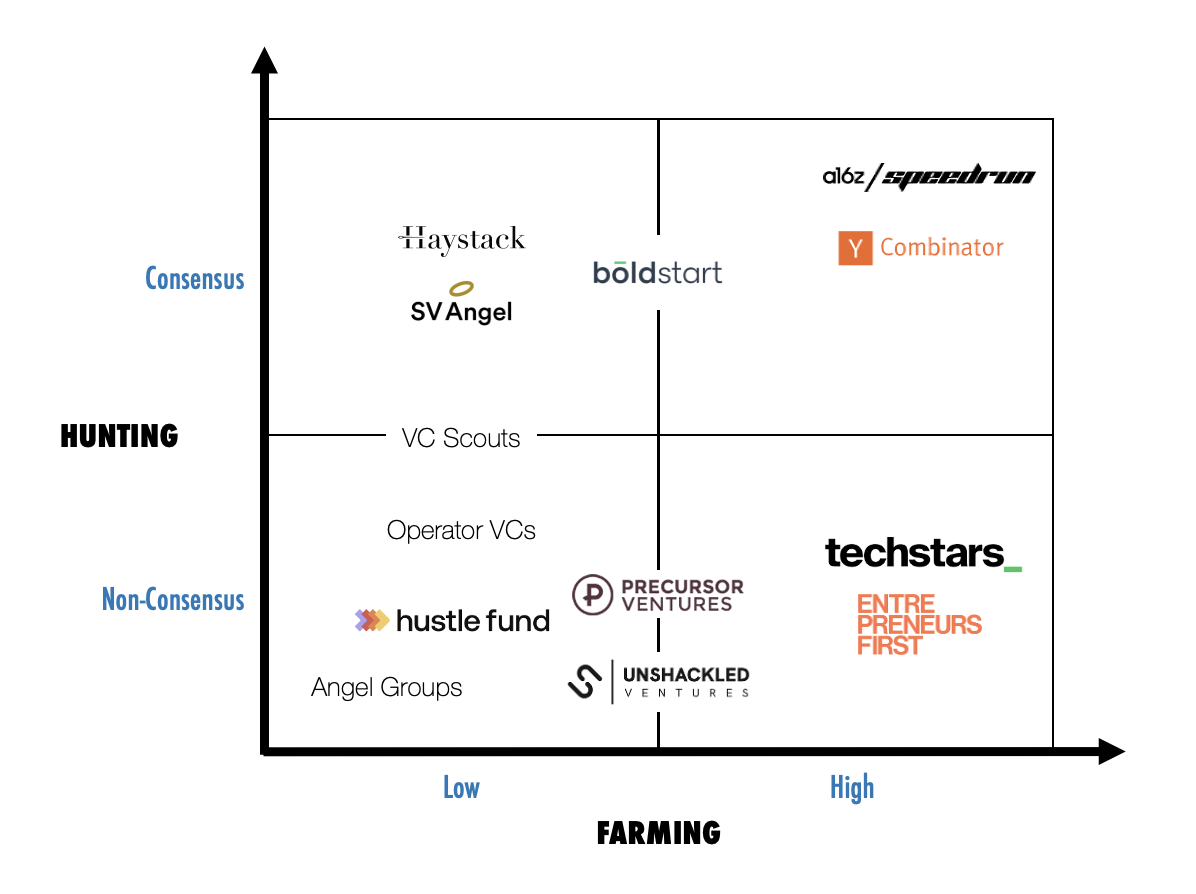

It’s important to understand that both of these are valid investment strategies that can lead to great success. Not only that, you can find investors who do both to varying degrees at almost every stage of investment. Consider this map showing a selection of pre-seed investors:

On the far right, you have accelerators. In the middle, are “hands-on” pre-seed funds (of which there are many). On the far left, you have hands-off investors, scouts and angel groups.

The Different Types of Farmers

You might be a bit confused looking at the above image, particularly given that many of the investors on the left side of the chart are known to be “very helpful” to portfolio founders. So let me specific about what I mean by farming. I consider a VC with a high degree of farming as one who regularly communicates with a founder (on at least a weekly basis) and provides hands-on help from the point at which they invest through at least the completion of their next round of funding. Accelerators and incubators typically have the highest degree of farming.

Investors with a low degree of farming might still be incredibly helpful, but that help is generally less frequent and/or lower touch. It might come in the form of on-demand introductions to potential customers, partners and follow-on investors or through “one-to-many” services.

Here is a very non-scientific ranking of the different types of VC farmers:

Passive Investors - After they invest, you rarely if ever hear from them (except occasionally in response to an investor update). Some can be very helpful with introductions and expertise but, generally speaking if you don’t call them, they won’t call you.

Automated Investors - These investors provide access to a selection of one-to-many resources (prerecorded videos, tutorials, webinars and online communities). Almost every email you get from them is from an automated system. One-on-one help is rare.

“Our Partners are Very Important People” Investors - These investors present as farmers — they often talk a big game about how they support portfolio companies — but after the deal is done, your point-of-contact suddenly switches from a partner to an associate or another lower-level member of the team. This approach is typically borne from VC firms trying to prioritize the “very important” partners’ time for hunting, as well as supporting the development of junior employees at the firm. While that sounds great on paper, it often feels like a bait-and-switch to portfolio founders (particularly when the “value-add” is provided by generalist team members with little or no real-world experience).

Board-Centric Investors - This category comprises a significant percentage of smaller VC firms (those with little or no support staff). Founders have a direct line-of-communication to their board partner (the partner who led the investment), but have little if any contact with anyone else at the firm. The board partner is often very hands-on, but the value provided is entirely dependent on what that individual brings to the table.

“We’re All Here for You” Investors - This is the next step up the farming ladder for smaller firms. In this case, founders have a direct (if infrequent) line of communication to all of the partners at the firm The board partner takes the lead on most matters, but the culture is such that founders are invited to reach out to any partner if they think they can help. Foundry Group (who invested in DataHero) had this approach — and I’ve always felt it to be the best strategy for small firms to take.

“We’re All Here for You” Investors II - Many mid-sized VC firms leverage analysts and associates to provide additional value add, like helping with research, market studies and financial analysis. The key difference between this category of VCs and “Our Partners are Very Important People” investors is that the associates/analysts provide services in addition to what the partner bring to the table instead of as a replacement for it.

Investors with a “Platform Team” - VCs with a platform team take the idea of additional support one step further by hiring experienced subject-matter experts to provide specific services to their portfolio companies. These hires can include recruiters, marketers, designers, media experts and even technical resources. Some of the larger traditional firms (most famously a16z) employ hundreds of people on their platform teams.

“We Have a Program” Investors - At the top of the farming pyramid are VC firms with “a program.” The difference between regular platform teams and platform teams at “We Have a Program” VCs is that startups who receive investment from the latter go through a formal program staffed by members of the platform team (as opposed to just receiving ad hoc support). Accelerators are the most well-known in this category, but an increasing number of traditional firms now have some form of post-investment programming (ranging from large firms like a16Z and Sequoia to smaller ones like Conviction).

(Strictly speaking, venture studios are at the tippy-top of the farming pyramid, but since most don’t invest in startups that are already up and running, I’ve omitted them from this discussion.)

How To Identify Hunters vs. Farmers

If all VCs seem to use the same, generic “value add” language when talking about their fund, how can you tell if they’re a hunter or a farmer? By listening to the subtleties in how they describe their approach.

In my experience, there are two topics where you can usually tell how a VC thinks about hunting vs. farming:

How the describe the founders they invest in

How they describe what they bring to the table (why they’re special / different / better than other VCs)

1. Who They Invest In

When describing the types of founders they invest in, hunters often use language that hints at pedigree and exclusiveness. Farmers, on the other hand, tend to emphasize the fact that they back founders from a variety of geographies, backgrounds and experiences:

| Hunters | Farmers |

|---|---|

|

"We only back the best founders" "We're looking for the top founders." "We invest in the top 1% of founders we meet." (Note: most VCs invest in about 1% of the founders they meet, but hunters often go out-of-their-way to make that point.) |

"We back founders from across North America." "We invest in founders from a variety of backgrounds." "We're less concerned with where you went to school and more interested in what you accomplished there." "We invest in founders from overlooked geographies." |

2. What Their Value-Add Is

When describing what their differentiation / value-add is, farmers tend to describe what they do (specific services / support offerings that they provide founders post-investment). Hunters, on the other hand, often focus on who they know.

| Hunters | Farmers |

|---|---|

|

"We know all of the top Series A investors." "We can introduce you to almost any C-level executive in your industry." "We host an annual CEO summit that brings together all of the founders in our portfolio with [insert celebrity CEOs here]." "We regularly host intimate/curated founder dinners with key industry stakeholders." |

"We facility monthly webinars with CEOs / CTOs / CROs across our portfolio to discuss specific topics." "We have a regular speaker series with subject-matter experts." "Each quarter, we host a fundraising bootcamp for companies preparing to raise their next round." "We have a number of resources on our platform team at your disposal. For example, we have a head of recruiting who can help you with executive hiring...." |

VCs can generate returns from almost any combination of hunting and farming. Which makes it essential to think in advance about what your ideal investor looks like.

Do you want a hands-on investor that will coach and mentor you through the next stage?

Do you feel confident in how to get from A to B, but need help with introductions?

There’s no right or wrong answer here, which makes diligencing a potential investor so important.

So when it’s your turn to ask an investor questions, turn the tables on them and ask the go-to question that so many VCs use:

“Why are you doing this, when there are so many other things you could be working on?”

“No, really. Why is this the thing you’re dedicated the next 10+ years of your life to?”

Then sit back and listen. You’re likely to learn more than anything you’ve read about them online.